Friday, April 28, 2017

Wednesday, April 26, 2017

Setting up a Successful Home Repair Budget

Many people will become first-time home buyers this spring. Those buyers are probably running the numbers now: This much for the mortgage, this much for property tax, a bit more for utilities….

Some of them will get renovation loans that allow them to rehab a fixer-upper and make it fit for fine living, but many won’t think to include the cost of ongoing maintenance as they plan their new budgets.

The adventure of buying a home was one that my husband and I approached with great excitement. We were ready to dive into gardening, outdoor entertaining, having a dog, and creating a space that was all ours.

Like many first-time home buyers, we had a lot to learn. In addition to delving into our personal finances, we studied up on things like mortgage insurance, flood zones, and - after a particularly revealing inspection on a home we didn’t end up buying - foundation types.

One thing that didn’t come up in our new-homeowner education: Budgeting for home repairs.

While unexpected home repairs can strain almost any budget, being prepared for these inevitable costs promised deep peace of mind.

We wanted to be the kind of homeowners who were prepared to replace a water heater or repair a roof without pulling out our credit card, so we began researching how much we should save each month to keep our home safe and sound.

As part of our research, we tried out two different methods of estimating home-maintenance costs, and set up a successful home repair budget.

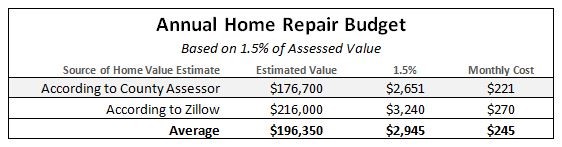

Option 1: The assessed-value method

Many experts advise setting aside between 1 percent and 4 percent of the assessed value of your home each year for repairs and maintenance. Maintenance costs for homes that are aging, remotely located (like island homes), or lavishly trimmed out with features like swimming pools can run toward the higher end.

Our home didn’t fall under any of these categories, so we chose 1.5 percent (one of the most commonly recommended rates) when we set up our estimate.

The assessed value (which forms the basis for property taxes) can vary a lot from the market value of a home. Knowing this, we also used our home value on Zillow to create our estimate.

This method was incredibly easy, but it didn’t give us complete peace of mind. Three major factors led us to take a deeper look at our actual home-maintenance costs:

- Assessed values are not always accurate.

- Home values can be affected by factors that are completely unrelated to actual repair costs (like the quality of the school district).

- The 1- to 4-percent savings rate range suggested by experts left us with some reservations.

Our specific situation gave us additional reason to doubt the assessed-value method of estimating. Because we are close to great amenities like a commuter rail station and a walkable historic downtown, we could own a much larger home just a half hour away with a lower assessed value. This much larger home would be more expensive to maintain than our cozy abode, but a savings rate based on assessed value would have us putting aside less money. The only way to ensure our peace of mind was to test the accuracy of this repair-cost estimate.

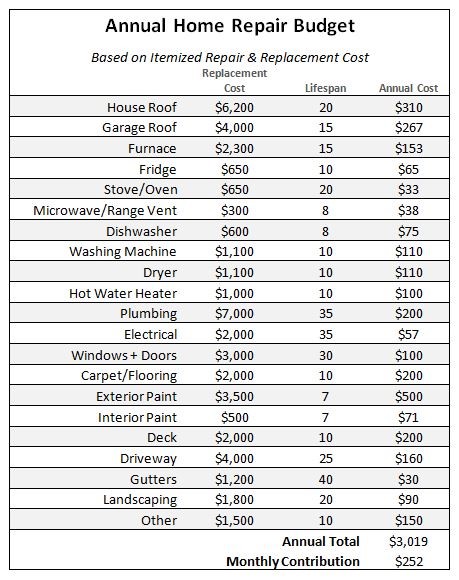

Option 2: Itemized project costs

Testing the accuracy of our home-maintenance budget required figuring out the cost of individual home repairs, and the lifespan of things like paint jobs and furnaces.

Here are a few factors we kept in mind as we put together a second estimate based on itemized costs:

- We live in an area with fairly high cost of living, so services aren’t cheap.

- Our house is very small (just 790 square feet!) so many repairs are less expensive.

- We usually buy our appliances “like new” from an outlet store.

- Our washer and dryer are in an extremely small space, and would need to be replaced with premium space-saver appliances.

Overall, this approach to budgeting was all about creating a customized savings plan that was specific to our needs. Here’s what we came up with:

Finding the facts

We are not experts in home construction and repair. When we weren’t sure how much to estimate, we used the Home Advisor True Cost Guide or talked with experienced friends.

We also didn’t need this budget to cover the cost of small expenses like lawnmowers or minor repairs. We knew we would use our everyday spending money to cover these less significant expenses, and save our home repair dollars for when we truly needed them.

A customizable solution

The beauty of a customizable solution like this one is that we can update our savings goals whenever we have new information about our home. If we discovered that our roof should be replaced within five years, we could change the lifespan and instantly update our monthly savings goal.

This method would be especially helpful if we owned an older home with several pressing repair needs.

What did we learn?

After all the time-consuming work of putting together the itemized estimate, it came out surprisingly close to using the assessed value method. This was especially true when we used our home’s market value instead of the value assigned by the Assessor-Treasurer’s office.

Unless there are dramatic fluctuations in the housing market, we’ll be setting our savings rate based on our home’s estimated market value in the future. We’ll also be sure to update our savings goals each year to make sure the amount we’ve budgeted is enough to keep up with inflation.

If we decide that something more than plain-Jane home maintenance is in our future, we’ll set aside a bit more to allow us to pay for remodels or renovations.

These tools together helped us set up a successful home-repair budget. The money we contribute to our home-repair fund each month is a small price to pay for peace of mind.

Ready to set up your customized home-repair budget? Download the Home Repair Budget Tool to estimate the costs for your home using either of these methods.

Related:

- How to Build a Home Renovation Team You Can Trust

- DIY Updates That May Boost Your Home’s Value

- The Do’s and Don’ts of Home Equity Loans

Note: The views and opinions expressed in this article are those of the author and do not necessarily reflect the opinion or position of Zillow.

from Zillow Porchlight https://www.zillow.com/blog/set-up-home-repair-budget-215076/

Friday, April 21, 2017

Tuesday, April 18, 2017

Do You Qualify for Treasury Down Payment Assistance?

It’s spring, and some renters’ thoughts may turn to home buying. Then reality hits: Between paying off student loans, paying rent, and keeping up with other bills, they haven’t saved for a down payment.

Renters cite down payments as one of the biggest roadblocks to homeownership. So, if you’re a low- to moderate-income home shopper in California, Florida, Rhode Island, Tennessee, or Kentucky, you’ll want to pay close attention. These states (and a few others) have Hardest Hit Fund (HHF) money available from the U.S. Department of the Treasury, which helps eligible buyers with down payment assistance (DPA).

Each state DPA program has income, credit score, occupancy, property value, and location requirements. But they share a common goal: revitalizing hard-hit communities.

“Our goal is to stabilize the neighborhoods and housing markets in Tennessee that have not recovered as fast as other areas across the state,” says Ralph M. Perrey, executive director of the Tennessee Housing Development Agency, which offers $15,000 in down payment assistance to draw home buyers to 55 ZIP codes across the state.

Innovative offerings

Housing agencies in 18 states and the District of Columbia have been administering HHF money since 2010. Participating states were chosen either because they struggled with unemployment rates at or above the national average, or they experienced home price declines greater than 20 percent since the housing market downturn.

In the beginning, programs focused on homeowners in some type of mortgage distress. “Now, to help these communities, we’ve developed programs for other issues we face,” says Cecka Rose Green, communications director at Florida Housing Finance Corporation.

Florida, California, Oregon, and Michigan have made HHF available to seniors who can’t pay property charges on their home equity conversion (reverse) mortgages. Illinois is now using HHF to help underwater homeowners refinance to more affordable loans. And several states have launched HHF DPA programs.

Florida’s $188.4-million HHF DPA program has assisted 7,481 first-time borrowers across 11 targeted counties. Borrowers can request up to $15,000 for down payment, closing cost, and prepaid assistance toward a home purchase.

“With the housing market improving, helping people buy homes is strengthening demand in hard-hit areas, stabilizing home prices, and preventing future foreclosures,” says Green.

“These agencies are being creative and resourceful in working with the Treasury to continue to serve their markets,” adds Mark Spates, a Fannie Mae director. Fannie Mae is the leading purchaser of loans underwritten by state housing agencies.

When the money runs out

States have until the end of 2020 to spend HHF money - but how they allocate funds varies from program to program.

The Arizona Department of Housing has a $76-million Pathway to Purchase DPA program, which has helped more than 2,600 buyers in 17 targeted cities.

But on March 29, 2017 - approximately 12 months after launch - Pathway to Purchase ran out of money, and the agency will not refund it. However, buyers can still apply for DPA from the state’s self-funded program, notes Dirk Swift, homeownership programs administrator for the Arizona Department of Housing.

Don’t wait!

California, Florida, Rhode Island, Tennessee, Kentucky, and a few other states still have HHF DPA money for renters hoping to buy - for now.

“We’re not in a situation where we’re about to run out of DPA funds,” advises Green. “But they’re going pretty fast.”

If you plan to purchase in an HHF state or want to learn more, contact your state housing finance agency, or visit the Hardest Hit Fund website to learn about local opportunities.

Looking for more information about mortgages? Check out our Mortgage Learning Center.

Top photo from Zillow listing

Related:

- Our Racially Divided Housing Market Is Changing, Thanks to Millennials

- What Is the Difference Between Interest Rate and APR (Annual Percentage Rate)?

- 5 Questions to Ask Potential Mortgage Lenders

Note: The views and opinions expressed in this article are those of the author and do not necessarily reflect the opinion or position of Zillow.

from Zillow Porchlight https://www.zillow.com/blog/treasury-down-payment-assistance-214856/

Monday, April 17, 2017

Wednesday, April 12, 2017

3 Updates That Helped Tyler Blackburn Create His Dream Backyard

When “Pretty Little Liars” star Tyler Blackburn purchased his first home, in Los Angeles’ hip Los Feliz neighborhood, he knew he wanted to make some changes to create a space that would truly feel like his own.

One of the actor’s favorite aspects of the renovation is the new and improved backyard, finished just in time for his big 30th birthday party.

Here’s a look at three updates he made to achieve his dream backyard.

Take a dip

Where there used to be an expansive slab of concrete, Tyler put in a large pool and hot tub. Complete with water features, the pool and hot tub’s design makes it easy to slip from one into the other - the ideal combination for a cool evening in L.A.

A place to relax

To escape the not-so-cool Southern California sun, Tyler built a pergola off the back of his house. Under its shelter, he placed a patio sofa, hammock chairs, and a natural wood coffee table where he can enjoy his morning coffee with his cute pup, Dylan.

Puppy playground

Not wanting to leave Dylan out, Tyler dedicated a large portion of the previously grass-less yard to a grass patch for her to romp around on.

To celebrate finishing his dream backyard, Tyler hosted his friends and family for his 30th birthday. The party was made extra special by the presence of his grandparents, who Tyler lived with as a young child.

Sometimes all you need for the perfect milestone birthday is good food, the people you love, and your own backyard.

Photos by Rupert Thorpe

Related:

- Ashley Benson Lists Pretty Little Lair in the Hollywood Hills

- Five One-of-a-Kind Details From Chris Hardwick’s Home

- Designer Lookbook: Ryan White’s Los Feliz Modern Makeover

from Zillow Porchlight https://www.zillow.com/blog/tyler-blackburn-dream-backyard-214468/

Tuesday, April 11, 2017

Our Racially Divided Housing Market Is Changing, Thanks to Millennials

Kieran Killeen was astounded when he bought a home in Vermont in 2002, and its title barred minorities from living there unless they were servants.

They were empty words. Racial covenants are no longer legal.

But Killeen, who is white, did not like having even a defunct racist restriction on his home’s title. He worked with neighbors to have it removed from his and 121 other homes in South Burlington.

Such covenants were once encouraged by the government. The language on Killeen’s title matched that used by the Federal Housing Administration in the 1930s: “No persons of any race other than the white race shall use or occupy any building or any lot, except that this covenant shall not prevent occupancy by domestic servants of a different race domiciled with an owner or tenant.”

“It took 70 years to undo the paper trail of institutional racism,” Killeen noted.

Unfortunately, this is not just history.

Racial covenants and other practices from the housing market’s racist past carry forward in the form of segregated neighborhoods and diminished wealth. They laid the groundwork for the terrible financial toll that black and Hispanic communities, in particular, paid during the Great Recession. Even redlining, a common practice from decades ago in which lenders denied loans in minority communities, has made a bit of a comeback in the wake of the housing crisis.

Promising demographic trends could improve the outlook, but some say that’s not enough.

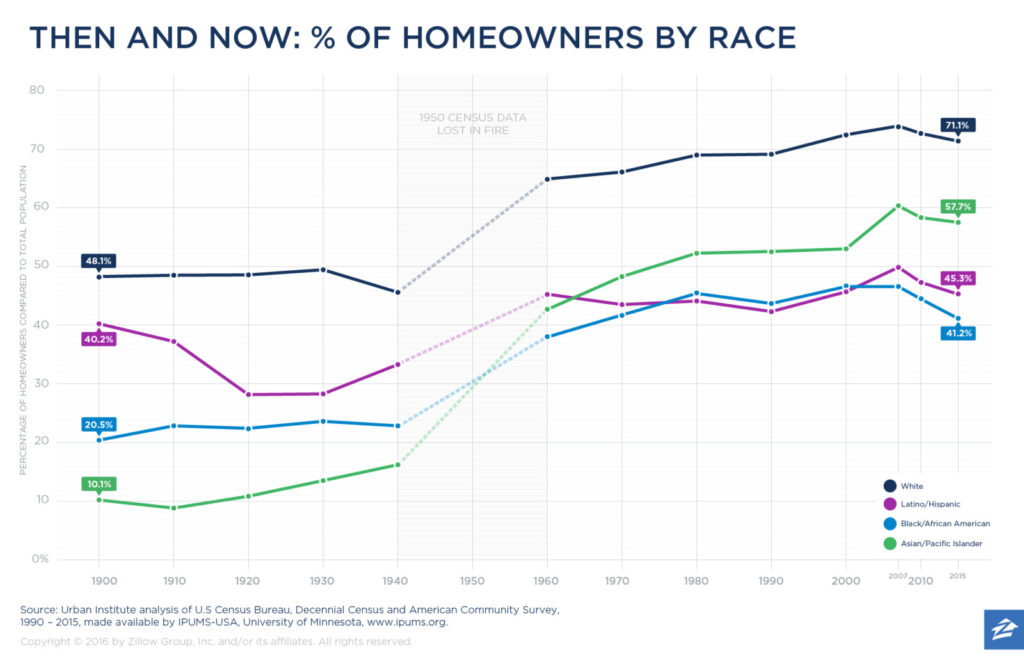

Millennials narrow the racial gap

For more than a century, there has been a persistent gap between white and minority homeownership rates. The most recent data show that 71 percent of whites own homes, compared with 41 percent of blacks, 45 percent of Hispanics and 58 percent of Asians, according to the U.S. Census Bureau’s American Community Survey.

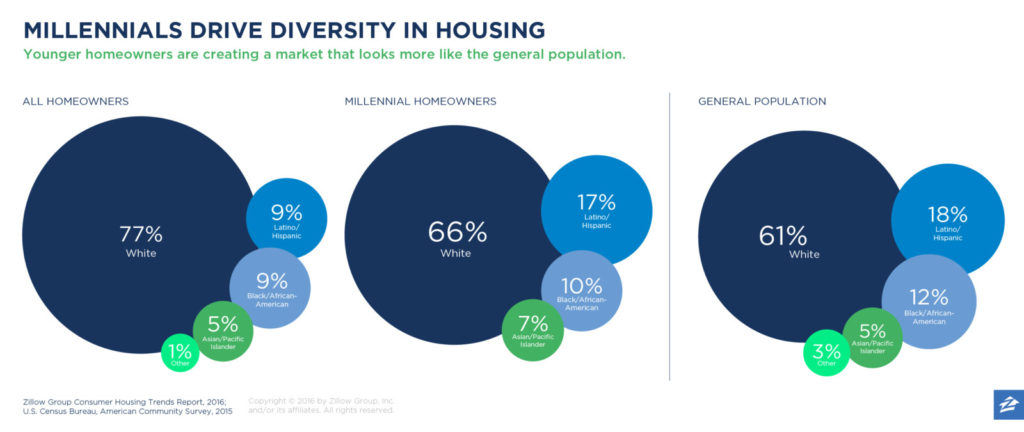

The good news is that the youngest generation of homeowners — millennials — is more diverse. And they’re driving the housing market more than people realized, according to Zillow Group’s Consumer Housing Trends Report.

“While minorities remain underrepresented among homeowners, that is changing as a younger, more diverse set of buyers enters the market,” said Zillow Group Chief Marketing Officer Jeremy Wacksman.

In fact, half of all home buyers are under age 36. Although the housing market as a whole skews heavily white — with black, Latino and Asian homeowners each representing less than 10 percent of the market — there’s greater diversity among millennials in general, and among millennials who own homes.

Only 66 percent of millennial homeowners are white - much closer to whites’ 61 percent share of the general population.

It’s also encouraging that Latinos and Asians have begun to narrow the gap between their homeownership rates and that of whites. But the gap between whites and blacks has widened.

Blacks face the longest odds

Aside from a run-up during the housing bubble, the homeownership rate for African Americans appears to be in a long-term slump.

The trend going forward is “uniformly worrying,” according to a 2015 report from The Urban Institute. “Erosion of homeownership for blacks threatens to undermine their ability to gain and maintain economic stability, not to mention build assets.”

That bleak picture follows decades of gains.

The economic fortunes of African Americans began to improve after the Fair Housing Act of 1968, when it became easier to challenge redlining, racial covenants and other forms of discrimination.

By the 1990s, blacks had finally established a foothold in the housing market.

However, during the housing bubble, many of them fell victim to mortgages that were unwise, and in some cases downright predatory, said Rolf Pendall, co-director of the Metropolitan Housing and Communities Policy Center at The Urban Institute.

“If you owned a house in a community where only 40 to 45 percent of people owned houses, and you had friends and neighbors and cousins, many of whom were less well off than you were, you might take money out [via refinancing] because you’re helping people get through,” he said.

At that time, even African Americans and Hispanics with strong credit were steered toward subprime or predatory loans, said Coty Montag, deputy director of litigation at the NAACP Legal Defense and Educational Fund. A former Justice Department attorney, she helped litigate a Department of Justice case against Wells Fargo for such steering that led to a $234 million settlement.

As a result, black and Hispanic neighborhoods were hit harder and have bounced back more slowly from the housing crisis.

“We look every day at sad faces when people are not able to get those loans,” said Antoine Thompson, national executive director of the National Association of Real Estate Brokers. It’s the oldest minority real estate trade association in the country, representing African-American and other minority real estate professionals, and it supports movement toward a new credit scoring model that takes into account rent and utility payments as well as non-traditional forms of income.

The Great Recession meant a tremendous setback, compounding earlier forms of housing discrimination.

Those historical practices included government-sanctioned redlining and racial covenants in the mid-20th century that kept blacks from buying homes and building wealth at the same time whites were.

The private sector also played a part back then, Montag said. “Real estate agents would not show African Americans homes in all-white neighborhoods, banks would refuse to grant African Americans conventional mortgages, and contractors could not get financial backing to construct homes for African Americans in white neighborhoods.”

There were also personal assaults, sometimes literally.

“White homeowners would actively discourage African Americans who tried to move to their neighborhoods,” explained Montag. “In some areas, there would be violence or other ways of discouraging new black neighbors.”

Being aware of the past’s injustices is the first step in understanding homeownership among African Americans today.

“Homeownership is the number one way wealth is built in America,” Thompson said. “Whether it was redlining by the government, issues related to African Americans who came home from World War II and did not have access to the GI Bill to go to college, or to government-sponsored loans that created the suburbanization of America: We cannot ignore those realities, which played a significant role in where we are today.”

Read more about African Americans and homeownership.

Latinos and the American Dream

The outlook for Hispanics is brighter, and surveys show they are more likely than any other racial or ethnic group to associate homeownership with the American Dream. A hefty 70 percent of Hispanic respondents told Zillow that owning their own home is necessary to living that dream, compared with 64 percent of Asian/Pacific Islander respondents, 63 percent of black respondents and 58 percent of white respondents.

“Homeownership is an aspiration for almost all Latinos,” said Lautaro Diaz, vice president for housing and community development at the nonprofit National Council of La Raza.

For good reason: Owning a home can be key to economic stability, better health and more education.

Hispanics face many of the same hurdles as African Americans, including a knowledge and familiarity gap regarding homeownership.

“If you have a parent and they own their home, they’re going to encourage their kids to do the same as soon as they’re in a position to do that,” Diaz said. “If not, the only way to get that incentive is an educational opportunity you go through, or a best friend — word of mouth is very impactful. People see success stories and think, ‘If they can do it, I can do it.‘”

Given Latinos’ lower incomes — they make $19,000 less than whites, on average — it’s particularly important for them to create a strategy for buying a house, sometimes as a family. “They have to channel their resources into buying a home and not necessarily sending money back to family in Mexico or Latin America,” Diaz said.

Read more about Hispanics and homeownership.

Knowledge as mortgage power

An aversion to debt also hurts minorities disproportionately.

Almost 20 percent of Americans are “credit invisible” or “unscorable,” according to the Consumer Financial Protection Bureau.

In low-income neighborhoods, that figure is closer to 45 percent — and there’s a divide along racial and ethnic lines. Only 16 percent of white consumers are “credit invisible” or “unscorable,” while 28 percent of black consumers and 27 percent of Hispanic consumers are.

“We meet people all the time who are excellent money managers but have no credit, and no idea that they have no credit,” said Ricki Lowitz, founder and executive director of the nonprofit Working Credit. She was a speaker at Zillow’s 2017 Economic Forum in Washington, D.C.

Some are immigrants who don’t trust American financial institutions. Some are African Americans who were told by parents and grandparents that if they didn’t use credit, they’d never go bankrupt.

“You have to borrow to build credit, and that’s a hard message,” Lowitz said.

Here’s the catch: Most landlords, utilities, cable and cell phone companies do not report monthly payment information to credit bureaus the way mortgage and credit card lenders do.

So if you’re saving to buy a house and find yourself tight on cash one month, pay the credit card bill before the cable. “If you’re 35 days late on the cable bill, no one knows. If you’re 35 days late on your credit card, it will be on your credit report for seven years,” Lowitz said. (However, if the cable bill goes to a collection agency, typically at about 180 days overdue, that is in your record.)

In the Asian community, there’s an added wrinkle: Some Asians are averse to debt because it carries negative connotations in their home countries, said Christopher Kui, executive director of the nonprofit Asian Americans for Equality.

Some are used to paying cash, or having to put 30 percent to 40 percent down on a home purchase, he said. If they have that large a down payment in the United States, the amount they borrow might be so low that they will not get the best interest rates from lenders.

“We do a lot of classes and workshops about how to save for a home, how you really have to take care of your credit history and delinquencies, and what the system looks for when you apply for a mortgage,” Kui said.

Read more about Asians and homeownership.

Changing the system

Kui and others suggest several ways the system could improve, including new credit scoring mechanisms and new mortgage products for people who don’t fit the standard home-buying mold.

One example is VantageScore, a project of the three major credit bureaus that uses a different model, scoring at least 30 million people who otherwise would be invisible to lenders. Not all low-income advocates love it, saying some measures can be discriminatory. But it’s an alternative for some people who have no score in the traditional system, said Alejandro Becerra, director of research at the National Association of Hispanic Real Estate Professionals.

“Banks could also take into account multi-generational income, seasonal employment and entrepreneurship like driving for Uber,” Becerra said.

He’d also like to see more lenders in minority communities. “Payday lenders and pawn shops have a presence there. There is still the need for a banking presence.”

It’s the kind of opportunity A.P. Giannini seized when he founded Bank of America — then Bank of Italy — back in 1904. At a time when banks catered mostly to the rich, this son of poor Italian immigrants built the largest bank in the country (by the time he died) by making loans to the working class. “Be ready to help people when they need it most…. It’s the helping hand on a dark day that folks remember to the end of time,” he advised.

Dedrick Asante-Muhammad, director of the Racial Wealth Divide Project at the nonprofit Corporation for Enterprise Development (CFED), believes that to make real headway, low- and moderate-income minorities need the same sorts of progressive economic programs — from mortgage insurance to subsidies for the building of middle-class suburbs — that whites enjoyed.

In the ’40s and ’50s, whites rocketed from 46 percent to 65 percent homeownership with those economic boosts. Minorities were explicitly left out via redlining, racial covenants and other practices.

Without aggressive intervention, by 2043, the wealth divide between white families and black and Latino families will have doubled, according to a study by the CFED and the Institute for Policy Studies. If white wealth remained stagnant, and black and Latino wealth continued to grow as it has for the past 30 years, it would still take black families 228 years and Latino families 84 years to gain parity.

The point of reaching more minority borrowers is not to make everyone a homeowner. Owning a home does not make sense for some people, including those who move frequently or who make so little money that they would have no financial cushion if they put everything into a home.

The aim is to even the playing field so that people with the means to own a home have a fair shot at it.

Related:

- Why Is My Lender Asking About My Race on My Loan Application?

- Black, Hispanic Mortgage Applicants Denied at Twice the Rate of Whites, Asians

- Black-White Mortgage Divide Starts Before People Even Apply

from Zillow Porchlight https://www.zillow.com/blog/millennials-diversity-housing-209688/

Monday, April 10, 2017

Thursday, April 6, 2017

Tuesday, April 4, 2017

How to Buy Property in Australia If You're From the U.S.

In addition to its white sand beaches and laidback lifestyle, Australia’s remarkably robust property market has long been a draw card for international buyers.

And the good news for United States citizens is that entering the market is relatively easy, and has many advantages beyond simply diversifying your investment portfolio.

Why Australia?

Stability

- Legislation and the Australian Prudential Regulation Authority (APRA) ensure that banks lend responsibly, reducing the likelihood of real estate bubbles.

- Australia’s population growth is outstripping the construction of new homes, creating a lack of supply and supporting prices.

Ease

- There is no need to set up a company in order to purchase Australian property.

- Obtaining government approval to purchase newly built dwellings is relatively cheap and easy.

- The National Consumer Credit Protection Act 2009 provides robust safeguards.

Choice

- There is significant apartment construction taking place in most major cities.

- U.S. citizens can also purchase commercial property, including farms.

10 things you need to know

- FIRB eligibility. All Australian property purchases made by non-residents must be approved by the Foreign Investment Review Board (FIRB). It is crucial that you understand the restrictions and fees imposed by the FIRB for different types of properties before you begin the purchasing process, or you may be unable to complete the transaction.

- New dwellings. Houses and apartments that have not been previously occupied (or have been sold by the developer and occupied for less than 12 months in total) are usually approved without conditions.

- Established dwellings. Non-resident United States citizens are generally prohibited from purchasing houses and apartments that have been previously occupied. The FIRB may grant exceptions on a case by case basis but it’s important to seek advice before you begin the purchasing process. Temporary Australian residents are normally allowed to purchase one established dwelling to use as their place of residence while in Australia.

- Find a conveyance. Almost all Australian property buyers use a conveyancer (or solicitor) to complete searches on the property, facilitate the transfer of ownership and review the sales contract.

- Find a buyer’s agent. A buyer’s agent acts as your advocate on the ground in Australia. She/he can provide you with nuanced market information, assist with listings searches and can bid on your behalf at auctions. You may decide you do not need a buyer’s agent.

- Get mortgage pre-approval if required. Australia’s regulatory environment means US citizens seeking mortgages must meet strict criteria. Before you begin searching for a property, apply for loan pre-approval from a bank. In general, you will need at least a 30 per cent deposit unless you are currently living in Australia or are married to an Australian citizen.

- Search for a property. Use reliable, comprehensive sources when searching for property listings. Domain is Australia’s leading source of property news, advice and has the country’s best property app. Want to know what a property is worth? Domain’s Home Price Guide tool provides estimates of each property’s value (similar to Zillow’s Zestimates) as well as previous sold and rental data. Want to know about local schools? Domain’s School Zones Report has the information you need.

- Arrange a property inspection. If you are seriously considering purchasing an established dwelling, engage a builder, surveyor or architect to inspect the property and identify any potential structural or maintenance issues.

- Auctions. Auctions are much more popular in Australia than they are in the U.S. However, new properties (which are easier to purchase if you are an international buyer) are typically listed at a fixed price. If you are buying an established property as part of a temporary visa and do find yourself at an auction be sure to understand the process and pick a strategy that works for you.

- Finalizing the sale. Once you have reached an agreement with a real estate agent or an apartment developer, be sure to follow these eight steps.

Fees you need to know about

There are five key fees and taxes US buyers will face when buying property in Australia. The biggest are Stamp Duty, FIRB Fees and land tax. You can read up on them all here.

Beware of scams

In general, Australia is a very safe place to purchase property, with solid regulations and a relatively stable market. However, scams do occur. In general, be wary of purchasing property that has not been advertised on a reputable website such as Domain or is being sold “off market” (i.e., without a real estate agent).

Related:

- Expert Advice for Chinese Home Buyers

- 5 Predictions for Renters and Home Buyers in 2017

- Moving From a Home With 2 Bedrooms to 3 Costs an Extra $450 a Month

Note: The views and opinions expressed in this article are those of the author and do not necessarily reflect the opinion or position of Zillow.

from Zillow Porchlight https://www.zillow.com/blog/buy-property-in-australia-214432/

Moving From a Home With 2 Bedrooms to 3 Costs an Extra $450 a Month

Thinking about moving this year? Whether your family is growing or you’re just looking for more space, upgrading to a home with an extra bed or bath comes with a premium in most metros.

To help buyers better understand their options this home-shopping season, Zillow identified how much extra “move-up” buyers could expect to spend on their mortgage if they were to upgrade to a similar home, but with just one extra bed or bath.

Nationally, families moving from a 2-bedroom to a 3-bedroom home can expect to pay $447 more on their monthly mortgage, according to Zillow’s Cost of Moving Up Report. That equates to a 50 percent increase in their monthly mortgage payment.

In many coastal markets, the cost is higher, around $500 extra each month - and in hot markets like San Francisco and San Jose, families can expect to nearly double their monthly mortgage payment, with the premium for moving up exceeding $1,600.

Buyers in the Midwest will see their dollars stretch much further. Families in Chicago, Cincinnati and St. Louis can expect to spend just $150 more on their mortgage when upgrading from a 2-bedroom to a 3-bedroom home. Cleveland offers the lowest premium out of all the metros analyzed, with move-up buyers paying just $74 extra a month to upgrade to a 3-bedroom.

“While deciding whether to move is a personal choice, understanding how certain characteristics like size, location or number of beds and baths can impact a home’s price can be hugely important when determining if a particular home is the right fit for you and your family,” says Dr. Svenja Gudell, Zillow chief economist. “Even though many families may be prepared to spend extra for a larger home, just how much more may come as a surprise, especially for those living in coastal markets.”

Bathroom count can also impact a home’s price. Nationally, upgrading to a house with the same number of bedrooms, but with one extra bathroom can cost buyers between $386 and $838 extra a month, depending on the home size. Given this premium, adding an extra bathroom to an existing home may be a cost-effective option for some families.

Curious about the cost of moving up in your area? Check out the interactive graphic on Zillow’s research page here.

from Zillow Porchlight https://www.zillow.com/blog/cost-of-moving-up-214404/

Going for Gold: Pro Snowboarder Shaun White Lists CA Home

Two-time Olympic gold medalist Shaun White just put a price tag of $7.995 million on his home in Encinitas, just outside San Diego, CA.

The professional snowboarder and skateboarder recently remodeled the 4-bedroom, 5-bathroom beachside abode, adding modern touches like custom accordion glass doors that open onto decks facing the Pacific Ocean.

Far from the snow-lined half-pipe that made him famous, White’s gated, multi-level home boasts ocean views from nearly every room. And when you’re done just looking at the ocean, stairs lead to the sandy California beach.

The bathrooms boast a simple, modern black-and-white color scheme: clean lines of pristine subway tile and white-and-gray marble countertops with silver accents. The master bathroom features a soaking tub for soaking up ocean views.

The black-and-white palette extends to the two-car garage, with a classic checkered floor. And don’t worry about stashing outdoor gear; there’s a separate storage room for boards of all kind (snow, skate and surf).

The athlete-turned-rock-musician bought the 3,500-square-foot home about 30 miles north of San Diego for $3.85 million in 2012.

The home is listed by Kathleen Gelcich of Sotheby’s International Realty.

Related:

- ‘Inferno’ Director Ron Howard Asking $12.5M for NYC Home

- Lauren Conrad Lists Pacific Palisades Home for $5.195M

- Check Out Ivanka Trump’s New D.C. Digs

from Zillow Porchlight https://www.zillow.com/blog/snowboarder-shaun-white-lists-home-214321/